Alibaba Earnings Preview: Can High Cloud Growth Offset Profit Bleeding?

Alibaba is set to release its financial results for Q4 of the fiscal year 2026 this coming Wednesday. Analysts anticipate that the upcoming financial report will reveal a significant divergence between the better-than-expected growth in the cloud business and substantial pressure on core profitability. The market focus has shifted from purely e-commerce GMV to whether AI-driven cloud revenue can offset the profit erosion brought by investment in computing power, as well as Alibaba's new positioning in the era of AI.

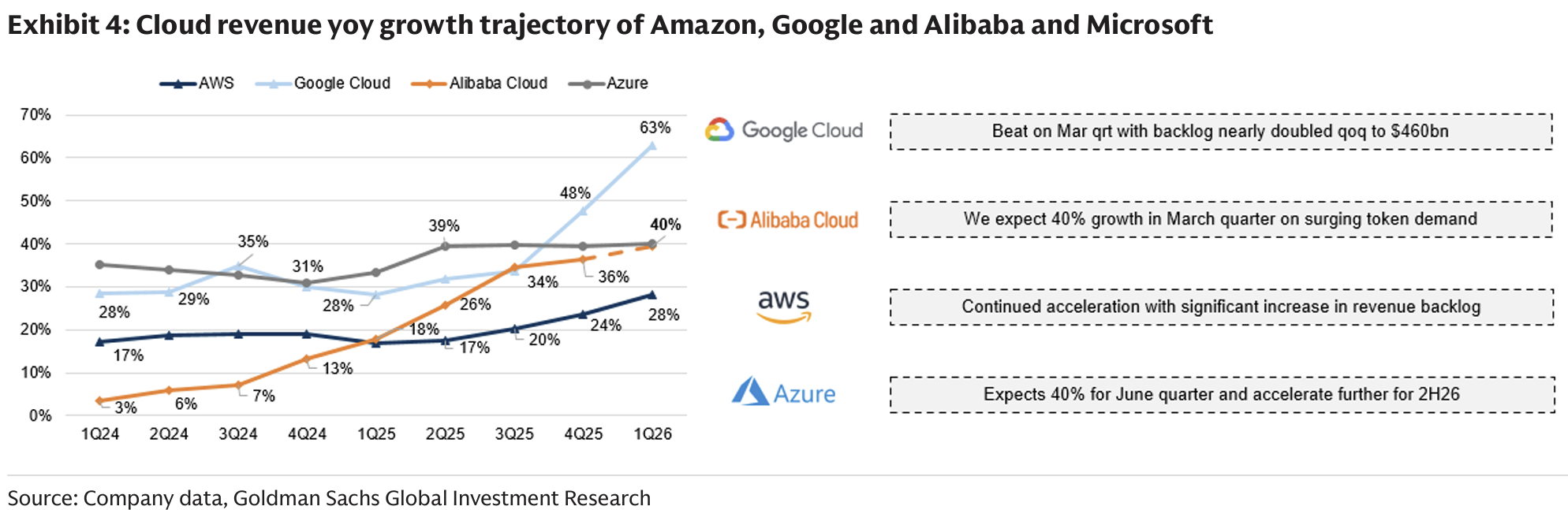

Revenue to Show "Structural Significant Differentiation"

Goldman Sachs forecasts a revenue increase of 4% for Alibaba in FY26Q4, but the adjusted EBITDA for this quarter is expected to plummet by 84% year-on-year to 5.2 billion yuan. This cliff-like pullback directly points to the company's cost-no-object investment in large model infrastructure. The core contradiction lies in the market's examination of "how AI restructures the valuation".

Analysts predict that customer management revenue, affected by new merchant policies, will only maintain a low-speed growth of 1%, with Taobao and Tmall experiencing a continuous bottoming out of profit margins amid defensive competition. The cloud business, however, has reached a critical turning point against the backdrop of a computing power shortage: driven by the demand for smart entity tokens, the growth rate of cloud revenue is expected to soar to 40%.

This reflects the company's shift from a volume-based pricing model to a business model with long-term contracts. According to Jefferies' analysis, Alibaba Cloud is strengthening its pricing power in the industry chain through model-as-a-service contracts.

However, this is only the tip of the iceberg. Goldman Sachs emphasizes that Alibaba is facing a strategic choice between "going all-in" or being "conservative": if it follows the path of American peers and adopts a zero-free-cash-flow model to aggressively purchase computing power, the profit and loss statement will further bleed. The current market consensus is that Alibaba will use the high growth of its cloud business to pay for AI investments, but whether this logic can appease Wall Street depends on the tone set for Capex during the earnings call.

Cloud Business Explosion Repairs Valuation Logic

This pain of profitability has been reflected in the valuation level, with Alibaba's current trading price corresponding to a price-to-earnings ratio for the following year's profits of only 18 times, a significant discount compared to Meta and Google.

Goldman Sachs believes that this discount offers an upward risk-reward ratio, provided the cloud business can deliver a 40% growth rate. Jefferies is more aggressive, noting that although Alibaba's stock price has fallen by 9% this year, based on the recovery logic of American cloud manufacturers, Alibaba is on the cusp of a valuation repair. The key is whether the market is willing to pay for the "cloud+AI" story, rather than getting caught up in the low single-digit growth of the core business.

If the logic of cloud price increases is confirmed, it will greatly repair the market's pessimistic expectations. The company's paper profits in

Content is for reference only, not financial advice.