Bank of America's Hartnett: AI is the biggest bubble since the railway bubble, but now is not the time to sell

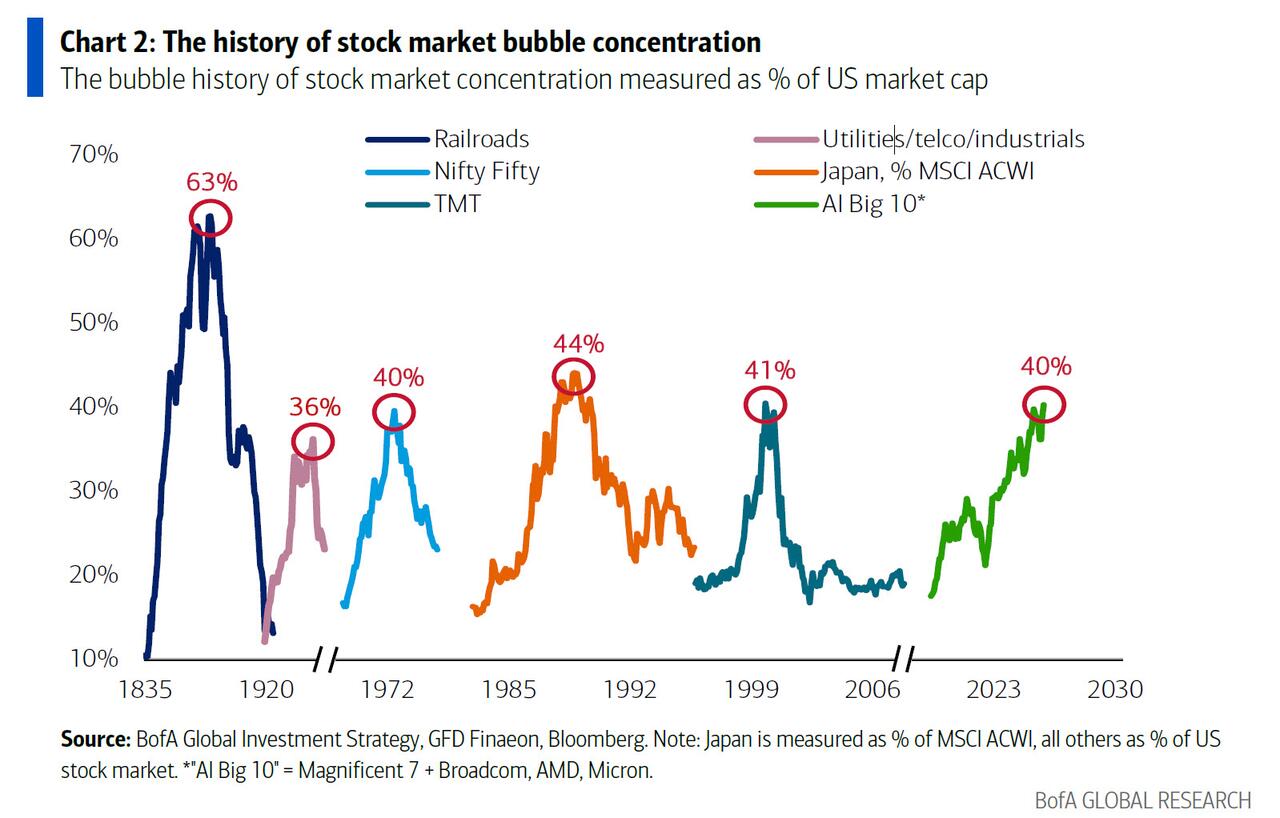

Bank of America's Chief Investment Strategist, Michael Hartnett, warned in the latest edition of the Flow Show report that the current AI market bubble has surpassed the "Roaring Twenties" of the 1920s, the Nifty Fifty of the 1970s, the Japanese stock market in the 1980s, and the internet bubble of the 1990s. If the upcoming mega IPOs are factored in, the AI sector's market valuation concentration will approach 48%, just behind the 63% peak during the railway bubble of the 1880s. Michael Hartnett summarized the current market sentiment as "strong price trends, retail mania, and low volatility—distinctive signs of a bubble." The Bank of America bull-bear indicator rose to 8.0 this week, triggering a sell signal for risky assets—a signal that has been triggered 17 times since 2002, with global stocks experiencing an average 2% to 3% pullback in the following 2 to 3 months, with the maximum drawdown reaching 15% to 20%. Meanwhile, the fund manager survey indicates that institutional positions and earnings expectations are at extremely optimistic levels, with a record monthly increase in stock allocations and cash holdings falling to 3.9%.

All Bubble Signals Lit Up

Hartnett believes that it is still too early to reduce positions now, despite frequent signals of a top, and has provided two waiting conditions: first, the historical super IPOs such as SpaceX and OpenAI are priced with a "banks won't allow market collapse before collecting billions in underwriting fees"; second, a significant policy tightening triggered after CPI rises to 4% to 5% in the coming months. He pointed out that the surge in bond yields has always been a signal of the end of prosperity and bubbles, and this week's 30-year U.S. Treasury yield rose to a 19-year high as a caution, but XBI touching $120 means that yields could still rise further, and XRT breaking through $85 means that the bond impact will be delayed.

Asian Export Inflation, Emerging Market Currencies in a Bind

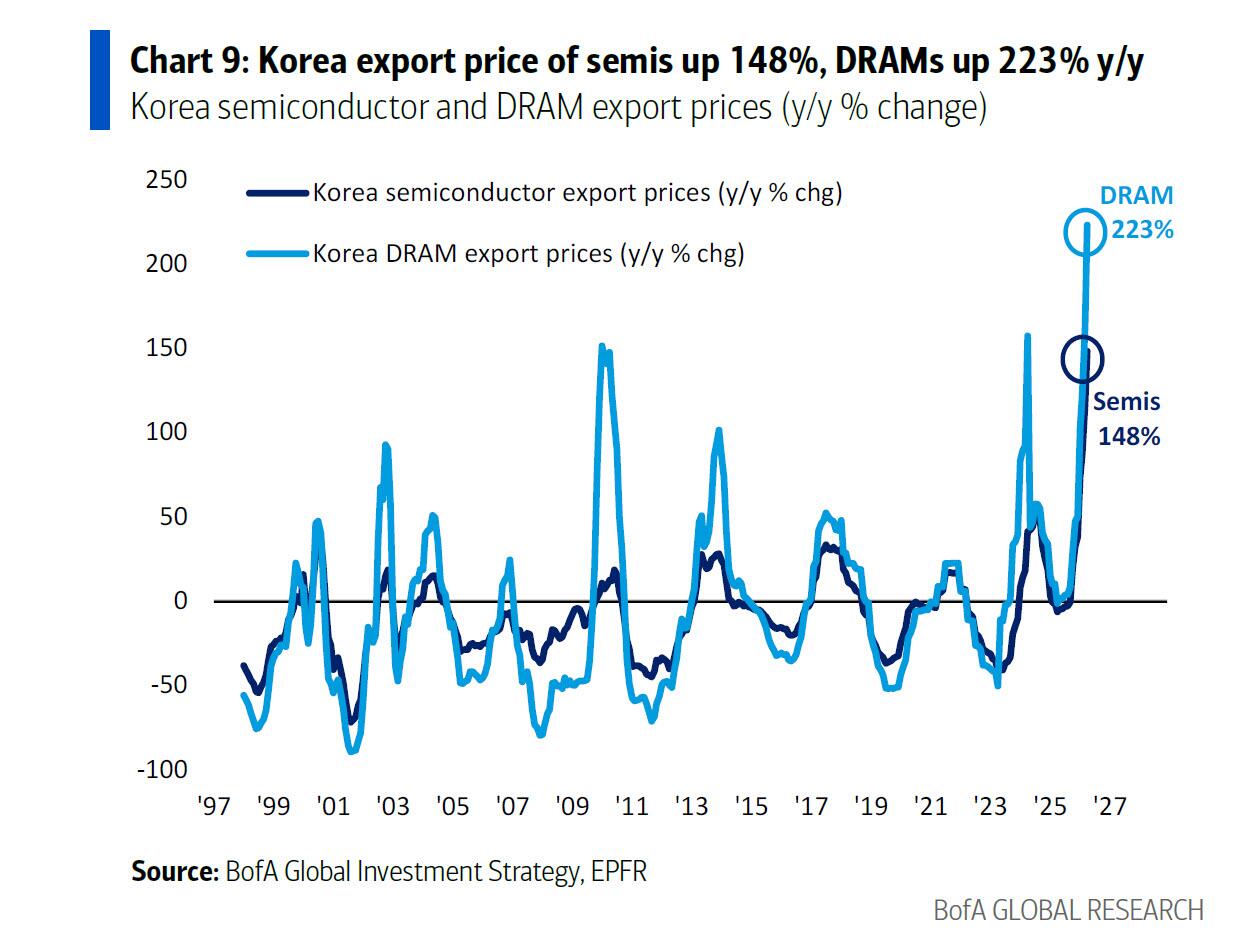

Geographically, Hartnett warned that Asia's technology industry, while aggressively expanding, is exporting inflation outward—South Korea's semiconductor export prices rose by 148% year-on-year, and DRAM prices skyrocketed by 223% year-on-year. Currency market risks are also accumulating in tandem: the Korean won lingered at a 30-year low, the Japanese yen touched a 35-year low, and the Indonesian rupiah and Indian rupee fell to historical lows. Hartnett warns that a surge in global capital costs historically impacts the periphery of emerging markets first and then spreads to the housing, consumer, and private equity sectors.

Capital Flows: Technology Absorbs Money, Emerging Markets Bleed

The capital flow data this week confirmed the above division: the technology sector saw a weekly inflow of $9 billion, the largest since October 2025; the U.S. stock market has seen a net inflow for 8 consecutive weeks; meanwhile, emerging market stocks have seen a net outflow for 6 consecutive weeks, with this week's size reaching $7.9 billion, the longest consecutive outflow since November 2024; cryptocurrencies saw a weekly outflow of $1.5 billion, the largest since February 2026.

After the Bubble, Who is the Best Contrarian Opportunity

Hartnett's structural judgment is that emerging markets and commodities are still in a long-term bull market; consumer stocks will be the best contrarian layout targets after the bubble bursts—currently, the equal-weighted consumer stocks relative to the S&P 500 have already dropped below the Lehman crisis low; the biggest winner in the second half of the AI trend will be small-cap technology applicators who break the monopoly pattern, just as history repeated after the collapse of the Nifty Fifty in the 1970s.

He concluded with a piece of client feedback, saying it all about the current market mentality: "We are fully invested, but we are worried."

Content is for reference only, not financial advice.