BCA: Stock-Bond Collision, Only Equities Downturn May End the Bond Bear Market

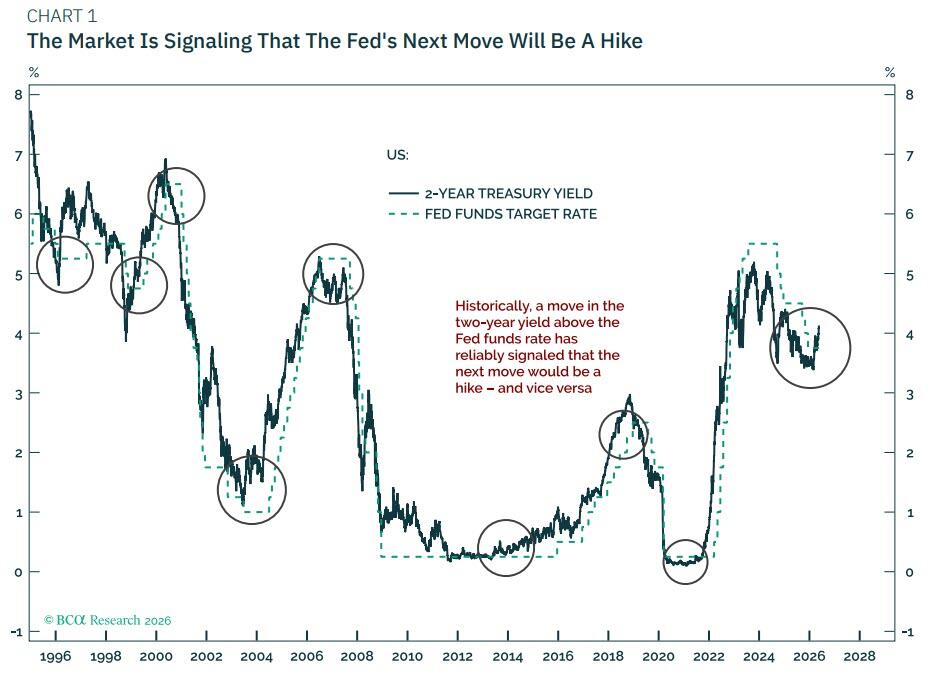

The pressure of interest rates has sent a clear signal on a technical basis. The 2-year U.S. Treasury yield has recently exceeded the federal funds rate again, triggering each instance of an interest rate hike by the Federal Reserve in the past 30 years. At the same time, the core CPI has continued to exceed 2%, while PPI terminal demand (excluding energy and food) has risen to 5.25% year-on-year in March, reaching an annualized growth rate of 6.6% in April over six months. BCA judges that the crisis in the Strait of Hormuz will not end in the short term, and the risk of oil prices rising is still significant, which means that U.S. Treasury yields do not have the conditions for a substantial decline.

The Federal Reserve is in an extremely passive position. Regardless of whether they choose to raise interest rates or keep things as they are at the next meeting, the reaction of stock investors will be negative. If they do not raise interest rates, the bond market may further sell off—because against the background of rising inflation and resilient economy, the longer the central bank delays, the greater the magnitude of interest rate increases needed in the future. A central bank that lags behind the inflation curve is bearish for both stocks and bonds.

The vulnerability within the stock market structure should also not be overlooked. While the S&P 500 index has reached new highs, the line chart has turned downward, with only 55% of the components standing above the 200-day moving average, and the implied correlation among components has dropped to its historical low. Excluding TMT, the S&P 500 is still far below the February high. BCA believes that the mean reversion of correlation will be the catalyst for a significant pullback in the overall index, and the widening of high-yield bond credit spreads has already issued a warning.

The scale of U.S. household stock ownership has reached a record 250% of disposable income, with a wealth effect that continues to stimulate consumption and AI capital expenditures. The data center investment of large-scale cloud providers will not stop unless their stock prices fall or the cost of equity financing significantly rises. BCA thus reaches the core conclusion that only a stock market decline can release deflationary forces in the broader economy to offset the inflationary shock brought by oil and food prices.

In terms of the dollar, BCA maintains its "Going Over Dollar" (G.O.D.) thesis. The dollar's equal-weighted index has recently shown weakness relative to similar global assets, with neither the S&P 500 nor the trade-weighted dollar outperforming, even though TMT has significantly outperformed the non-TMT板块. BCA advises investors to take advantage of the phased strength of the dollar and U.S. stocks to gradually reduce their allocation to U.S. financial assets.

Content is for reference only, not financial advice.