BoA Bull & Bear Indicator Triggers Sell Signal, Equity-Debt Divergence Continues to Widen

The current market trend closely resembles the melt-up at the end of 1997, and this pattern continues to unfold. Goldman Sachs data shows that bullish option positions have surged again, setting one of the largest chasing waves in recorded history. At the same time, the option skew indicator has dropped significantly, with downside protection quickly abandoned, and investors have almost no vigilance against severe downward risks.

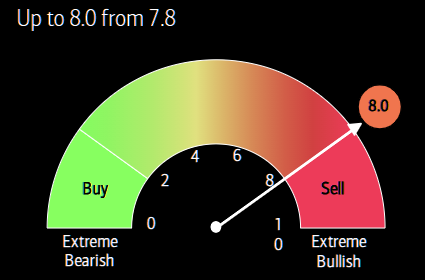

The Bank of America's Bull & Bear Indicator has just touched 8, officially triggering one of Wall Street's most closely watched contrarian selling signals. Bank of America strategist Hartnett wrote that the market has reached "consensus extreme bullishness" in terms of positioning and profits, and with the upward breakthrough in yields, it is advisable to take profits moderately; but he also pointed out that before the arrival of the historical IPO window, no one will actively reduce long positions, and the real policy tightening will come after the CPI hits 4% to 5% in the coming months.

The divergence between the bond market and the stock market is the most alarming structural risk at present. The divergence between the S&P 500 and the inverse of the US 10-year yield remains enormous, and the gap between the MOVE Index and the S&P 500 is also unresolved - how long the stock market can ignore the explosive increase in bond volatility is the core issue facing the market at present.

Inflationary pressures cannot be ignored either. Deutsche Bank points out that the current evidence overwhelmingly points to a cycle driven by capital expenditure and demand: the annualized increase in U.S. software CPI has exceeded 60%, capital goods inflation has risen to the highest level since the early 1990s, North Asian export growth has approached 40% year-on-year, and the three-month annualized growth rate is approaching a historical record. Samsung's latest salary agreement shows that the annual bonus for chip workers is up to $400,000, equivalent to eight times the base salary.

BCA Research warns that if the Fed is slow to raise rates against a backdrop of strong growth and inflation, it will be forced to implement more aggressive tightening later, and the Fed lagging behind the inflation curve is generally bearish for both stocks and bonds.

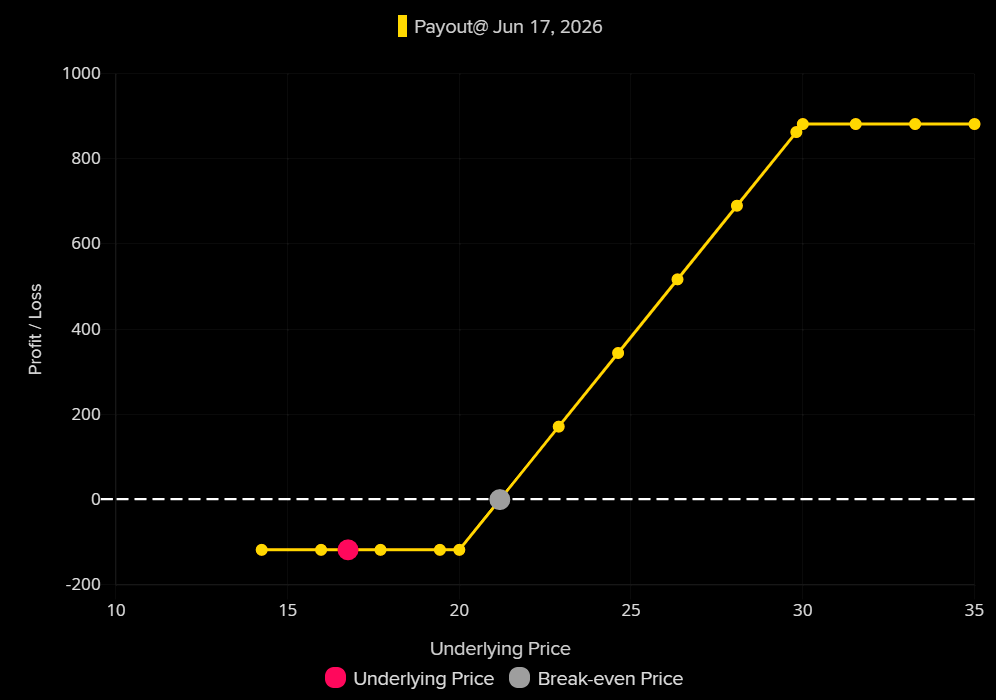

In terms of hedging, as the VIX approaches a kind of natural bottom, the attractiveness of VIX long strangle options is increasing. The VIX June 20/30 long strangle options currently offer a maximum payout ratio of about 8 times and are considered a cost-effective tail risk hedging tool at present.

Content is for reference only, not financial advice.