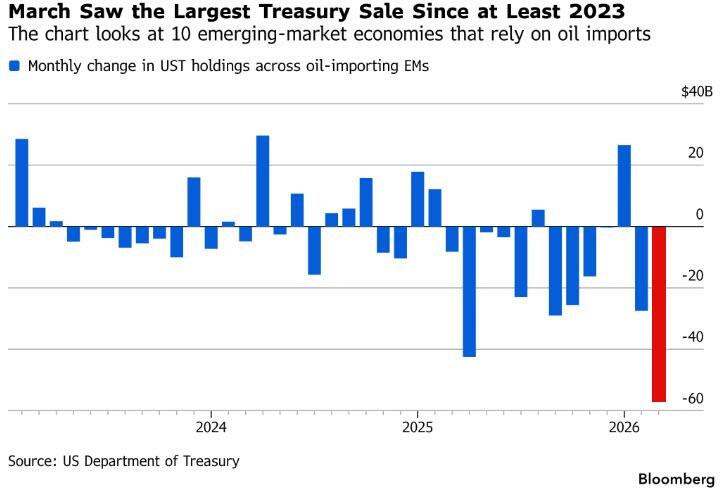

Emerging Markets Sell Treasuries at Record Level since 2011 in March

Bloomberg data shows that foreign holdings of U.S. Treasury bonds dropped significantly in March, with most of the decline attributable to valuation effects—down 1.7% for the month on the Bloomberg U.S. Treasury index, with market concerns about an Iran war driving inflation being the main source of pressure. However, in oil-importing emerging markets such as Turkey, China, and South Korea, holdings of U.S. Treasury bonds decreased by about $86 billion, the largest monthly drop since 2011, and of that, 56 billion was actively net sold, not just a valuation shrinkage.

China was the largest source of net sales in this round, but its motives are distinctly different from other emerging markets. While other emerging market currencies are under pressure, the renminbi has actually been strengthening recently, suggesting that Beijing's operation is more likely related to proactive asset allocation adjustments rather than passive foreign exchange intervention. Excluding China, the net sales of the rest of emerging markets still reached 22 billion dollars, also a record high for this dataset on a monthly basis.

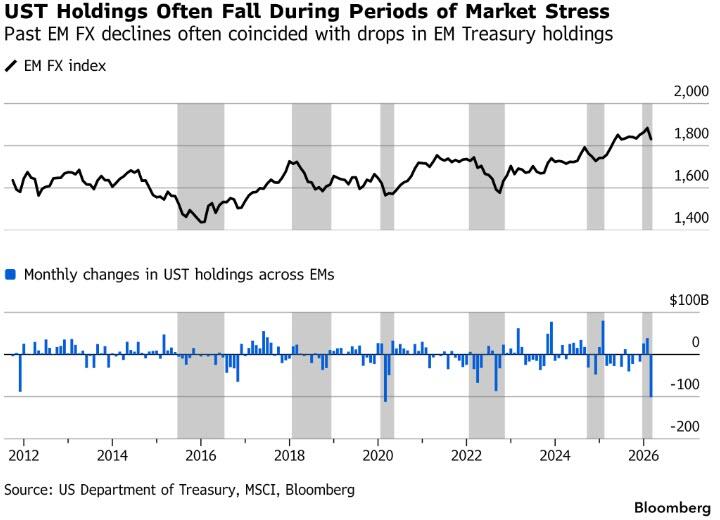

Historical patterns suggest that emerging market holdings of U.S. Treasury bonds often decline during market turmoil, and are not always correlated with the trend of U.S. Treasury bond prices. Comparing the monthly changes in holdings from 18 emerging markets with the MSCI Emerging Markets Currency Index reveals that decreases in holdings often occur in tandem with significant devaluations of local currencies—similar situations occurred in 2020 during the pandemic shock and in 2022 with the oil price surge, although U.S. Treasury performance was starkly different in both instances.

The implication of this structural risk is that if a war in Iran triggers a deeper energy crisis, the pressure on U.S. Treasury bonds will come not only from rising inflation expectations but also from the combination of passive sales due to the depletion of foreign reserves and currency intervention in emerging markets. The activation of both stress paths simultaneously is a tail risk that the current bond market needs to take seriously.

Content is for reference only, not financial advice.