Goldman Sachs: $800 billion AI capital expenditure contributes only 0.1% to US GDP

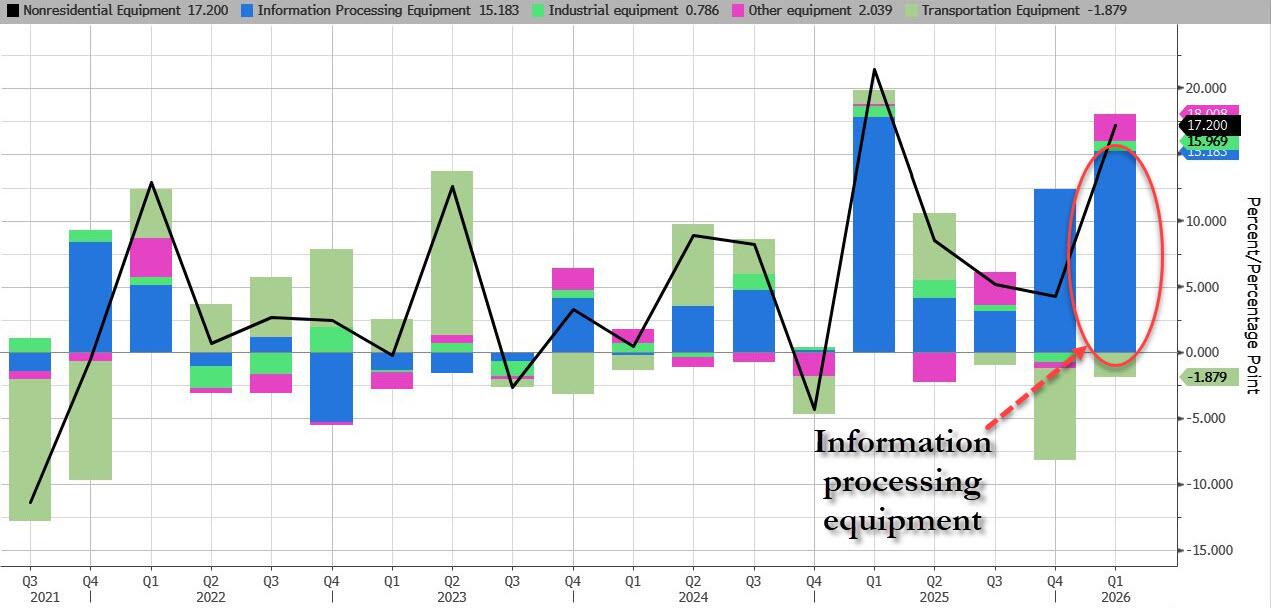

A month ago, the U.S. Bureau of Economic Analysis disclosed a set of eye-catching data: non-residential fixed investments contributed about 75% to the 2.0% GDP growth rate in the first quarter, with software and non-residential equipment investments both driven by AI at the core, contributing a combined 1.5 percentage points. In other words, three-quarters of the U.S. economic growth in the first quarter came from AI-related expenditures.

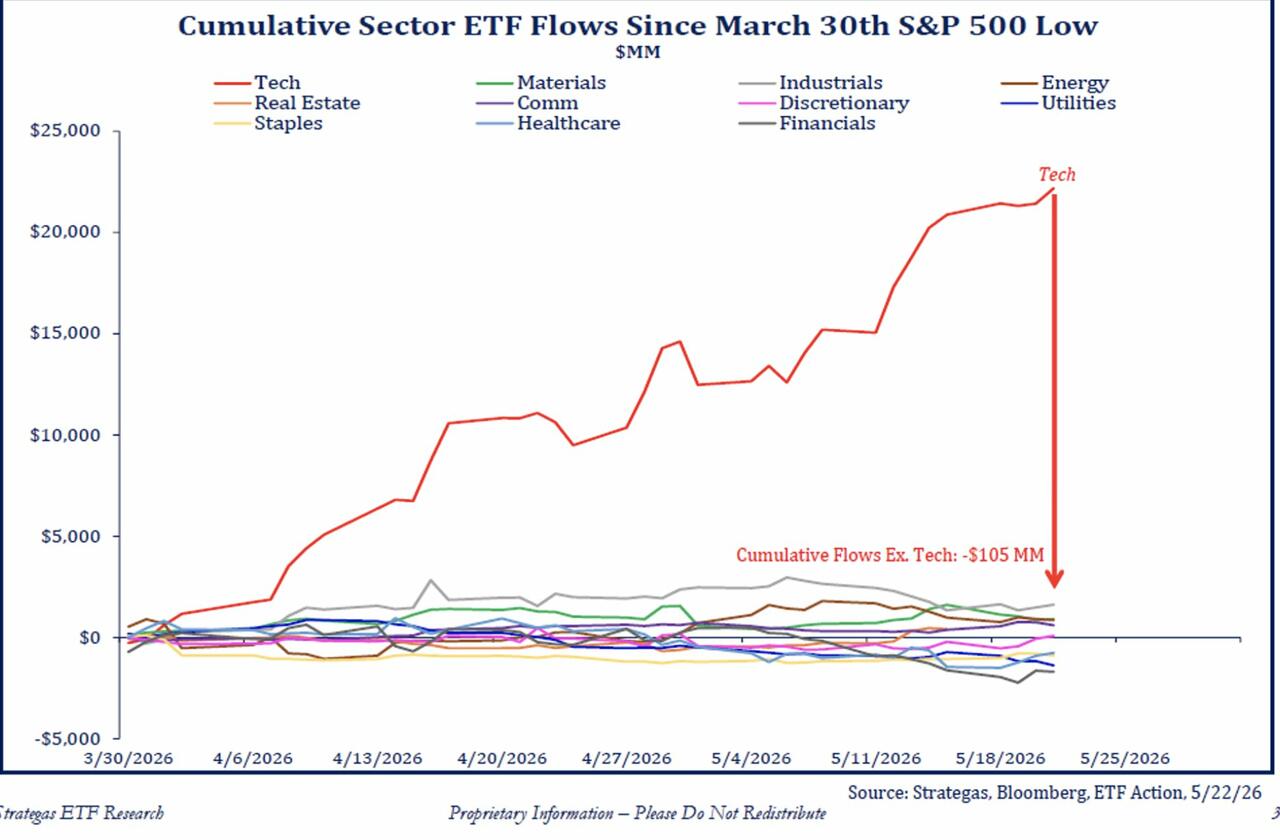

At the same time, since 2026, net inflows to technology sector ETFs have reached 23 billion USD, while the combined total for all other sectors is almost zero.

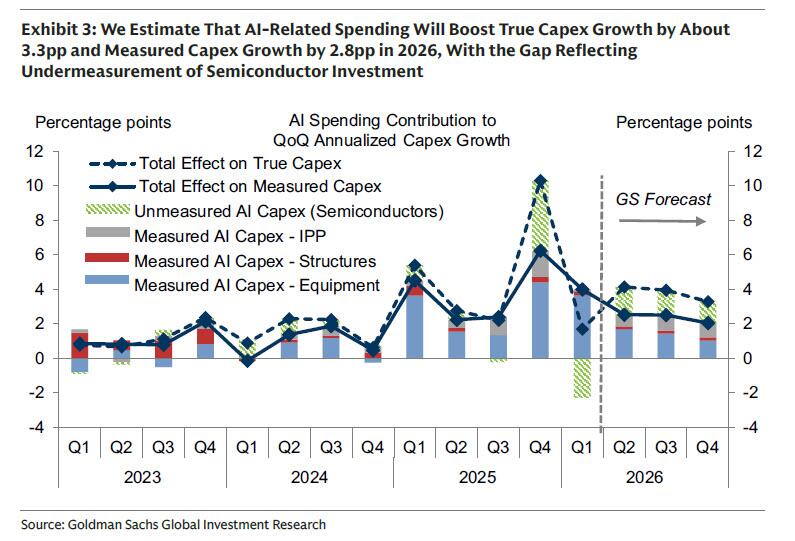

Goldman Sachs estimates that AI-related expenditures have reached an annualized scale of 650 billion USD in the first quarter, and will break through 800 billion USD by the end of the year, driving the growth of "real" capital expenditures by about 3.3 percentage points. However, this huge input has a very limited actual contribution to GDP—Goldman Sachs estimates only 0.3%, and even less, 0.1%, after accounting for statistical discrepancies.

The reason lies in two structural leaks. First, AI-related equipment heavily relies on imports, and the increase in investments is largely offset by higher import amounts, with the actual beneficiaries being core economies in the supply chain such as South Korea, Taiwan, and Japan. Second, the U.S. technology services export scale remains low, and intellectual property earnings like chip design are not fully captured in GDP statistics. This means that hundreds of billions of dollars in capital expenditures have a very limited direct economic stimulus in the United States.

Goldman Sachs also calculated scenarios of a reversal in AI investments. If capital expenditures contract significantly and focus on the equipment side, the impact on GDP is relatively manageable, as a synchronized drop in imports would partially offset it; however, if the contraction spreads to data center construction and intellectual property investments, it could drag down GDP growth by about 0.2 to 0.4 percentage points. What is even more alarming is that a sudden reversal in AI spending is often accompanied by widespread pressure on financial markets, and the actual impact may far exceed mechanical calculations. Goldman Sachs points out from this that the benefits and risks of AI capital expenditures show a clear asymmetry: large-scale investments contribute little to GDP, but if they contract sharply, they could trigger a recession.

In addition to AI, Goldman Sachs also assessed the impact of tax policies. The "Build Back Better Bill" expanded the capital expenditure tax deduction clause, and capital costs in industries such as manufacturing, transportation, and mining are expected to drop significantly, with early confirmation appearing in the first quarter data. At the same time, the headwinds from two policies are diminishing: the drag on capital expenditure growth from the withdrawal of subsidies under the Inflation Reduction Act and the CHIPS Act will narrow from about 1.0 percentage points in 2025 to 0.6 percentage points; the drag from tariff uncertainty will also decrease from 1.5 percentage points to 0.7 percentage points. Considering all factors, Goldman Sachs forecasts that capital expenditures in 2026 will grow by 7.8% on a year-over-year basis in the fourth quarter, with the whole year's GDP growth rate maintained at around 2.1%.

Content is for reference only, not financial advice.