Goldman Sachs Answers Top Five Fund Manager Questions: IPO Surge Looms, AI Aggressively Chasing Gains

Goldman Sachs' head of hedge fund business, Tony Pasquariello, released a report this week after visiting institutional clients in Boston and Toronto, compiling the five most concentrated issues that fund managers are currently concerned about, and providing judgments on each one.

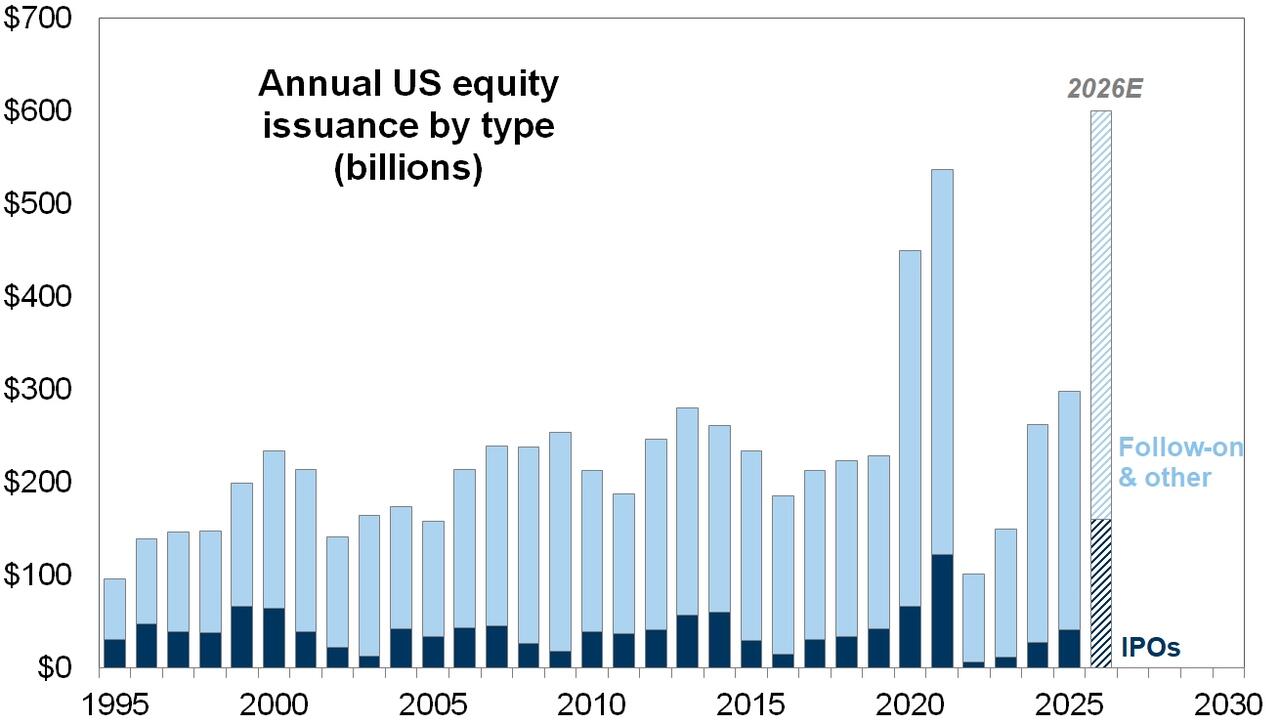

What is the scale of this year's stock supply? Goldman Sachs estimates that the total scale of U.S. stock supply in 2026 will reach $600 billion, with IPOs accounting for $160 billion, a nominal scale that sets a new record in modern market history.

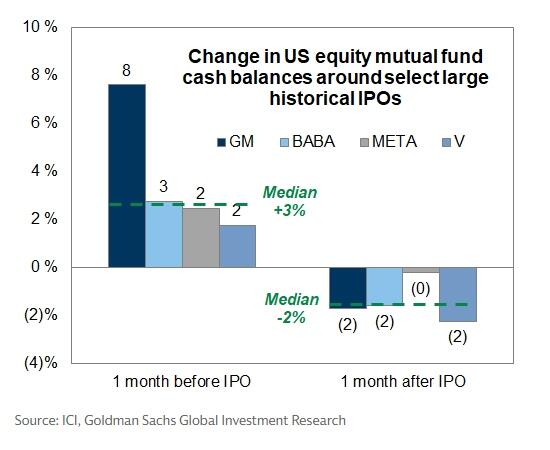

Can the market digest this supply wave? Pasquariello's answer is affirmative. After converting supply into market value ratio, the current level is not prominent compared with the dot-com bubble, the refinancing surge during the financial crisis in 2009, and the SPAC craze in 2021. He clearly expressed a positive judgment on the U.S. market's ability to absorb high-quality assets. Goldman Sachs trader John Flood added that there has historically been a pattern of mutual funds actively increasing cash positions before large IPOs, and currently cash represents 1.4% of assets. If an IPO with a market value of $1 trillion and a free float proportion of 10% is included in the S&P 500, the selling pressure caused on existing components will not exceed 5 basis points of their total market value.

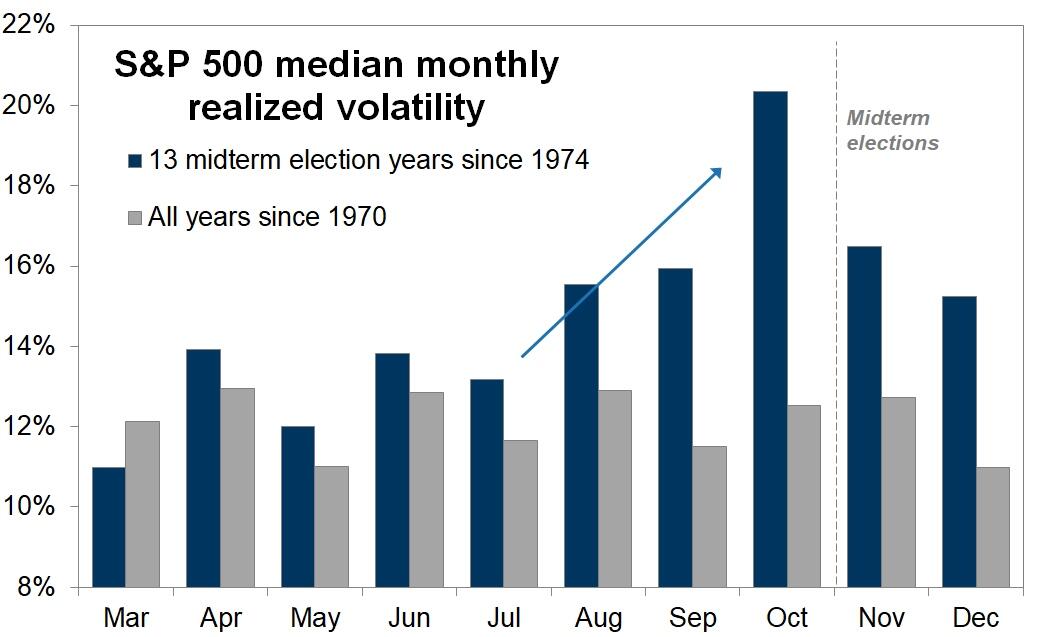

When will the market start paying attention to the midterm elections? Goldman Sachs cites strategist Ben Snider's research, noting that the U.S. stock market usually consolidates before the midterm elections, with actual volatility gradually increasing in the summer and peaking in October. This seasonal pattern implies that the volatility center in the second half of the year will systematically rise, which is worth incorporating into the risk management framework in advance.

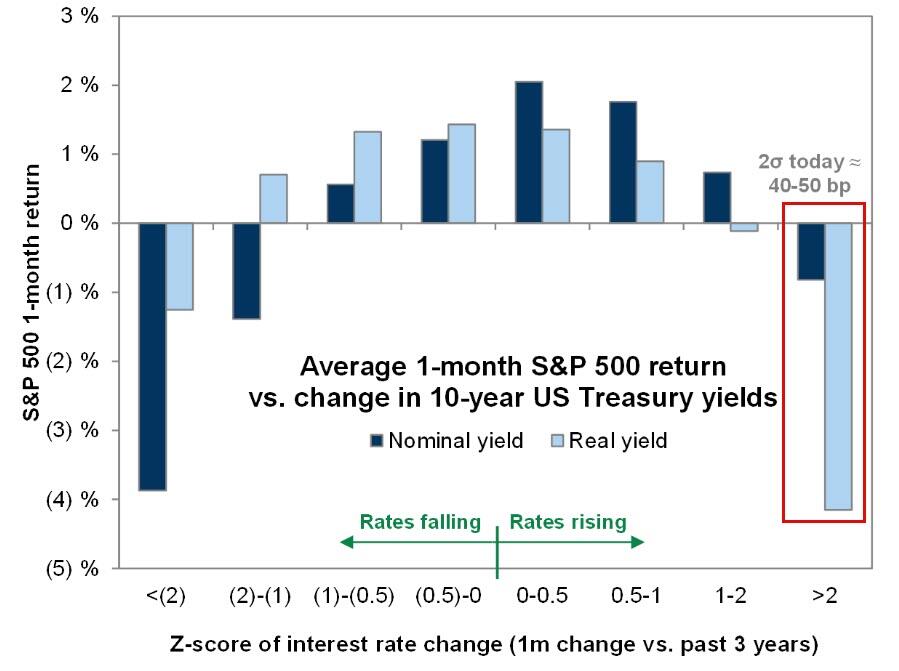

When will the upward interest rate trend truly start to hurt the stock market? Goldman Sachs provided a clear quantitative critical point: when the yield on 10-year U.S. Treasury bonds rises more than 2 standard deviations, or about 45 basis points, in a month, the stock market will begin to feel the pressure. Pasquariello pointed out that on Tuesday this week, the market was already very close to this threshold, and interest rate risk is not a distant assumption.

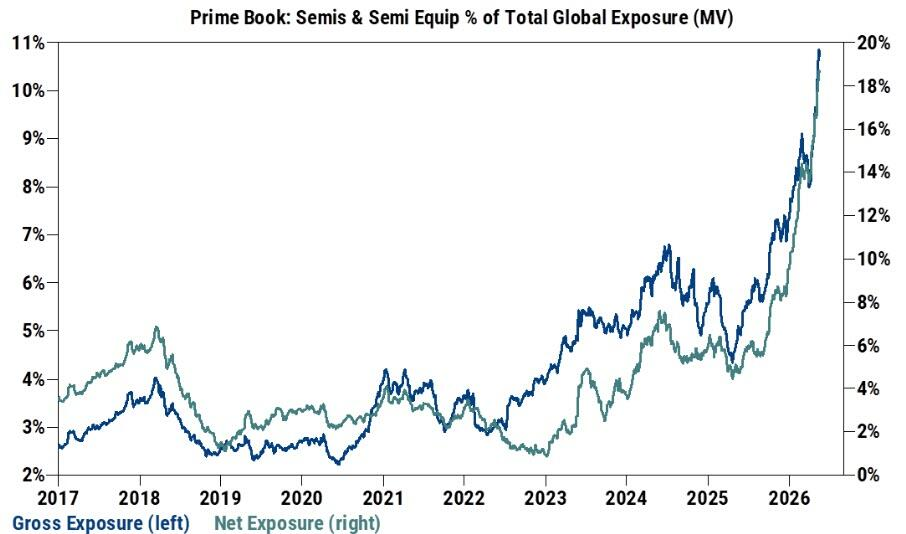

How aggressive is the market in chasing AI beneficiary stocks? Goldman Sachs Prime Brokerage data shows that the proportion of long and short positions in global semiconductor stocks relative to the total size of the book has climbed to an extremely high level. Pasquariello directly characterized it as "very aggressive," echoing Bank of America's Hartnett's warning about the over-concentration of the tech sector.

Content is for reference only, not financial advice.