Goldman Sachs Warns: Persistent Real Rate Increases, 'No Good Outcomes'

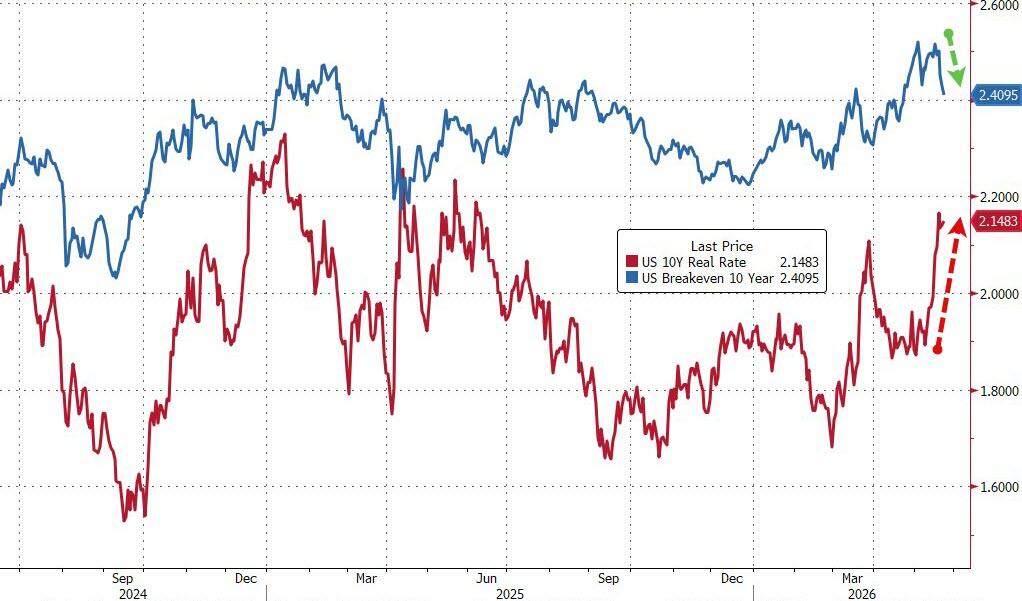

The nominal yield of the U.S. 10-year Treasury bond has recently risen by about 25 basis points, but the breakeven inflation rate has largely been anchored around 2.4%, with real interest rates having climbed to the 2.1% to 2.2% range. This pattern holds true in Europe and some emerging markets as well. Goldman Sachs characterizes it as a "tightening without inflation" — the rise in real interest rates tightens discount rates and financial conditions, but the quality of inflation is too low to trigger a broader transition to reflation. The driving forces behind this are the rise in term premiums, fiscal supply pressures, and the market's reassessment of the neutral real interest rate.

In a weekend macro conference call, Goldman Sachs' Senior Macro Advisor Dom Wilson noted that the real yield of the U.S. 30-year bond has reached historically rare levels. He emphasized that the current synchronized rise in stock markets and yields, which conventional models interpret as an upward revision of growth expectations, requires a "pretty strong growth story" to support such optimistic pricing. The AI capital expenditure supercycle may also exert a structural upward pressure on real interest rates.

The real risk lies in the shift of the logic driving real interest rates from "strong growth" to "fiscal sustainability concerns" or "the central bank needing to raise interest rates more aggressively." In that case, the market would face a completely different situation. Wilson cited the history of the sharp rise in long-term interest rates in the summer of 2023 as a reference - at that time, financial conditions tightened noticeably, carry trade strategies came under pressure, emerging market assets were impacted, and long-duration stocks and rate-sensitive assets (such as real estate and consumer goods) were at the forefront.

On the currency front, Wilson believes that under the backdrop of broad-based rises in global yields, it is difficult to judge the direction of the U.S. dollar, but if the aforementioned risk scenario comes true, the logic for the U.S. dollar to strengthen against the Japanese yen is the clearest, and some emerging market currencies will also face pressure.

The central bank's response will be a key variable. If the Federal Reserve clearly signals rate hikes, it could help anchor long-term real interest rates, but the pressure will shift to the short end, and the dollar could strengthen as well. If the Federal Reserve is hesitant, the pressure on the long end will continue to accumulate, the yield curve will steepen further, and long-duration assets and emerging markets will continue to be under pressure.

With the breakeven inflation rate now re-anchored, it provides some support for easing expectations in the short term. But Wilson's conclusion is straightforward: as long as real interest rates remain high, the future direction of the market will entirely depend on the trajectory of real interest rates themselves.

Content is for reference only, not financial advice.