Inflation Shock Ignites Bond Market, Goldman Warns of Equity and Bond Double Whammy

Goldman Sachs' recently released Global Asset Allocation Strategy Report indicates that due to the latest U.S. inflation data exceeding expectations and strong real economic activity data, it has triggered a sharp sell-off in the global bond market. Against the macro backdrop of more reflationary characteristics, U.S. Treasury yields have soared significantly, causing a noticeable spillover effect on overseas bond markets such as those in the UK and Japan.

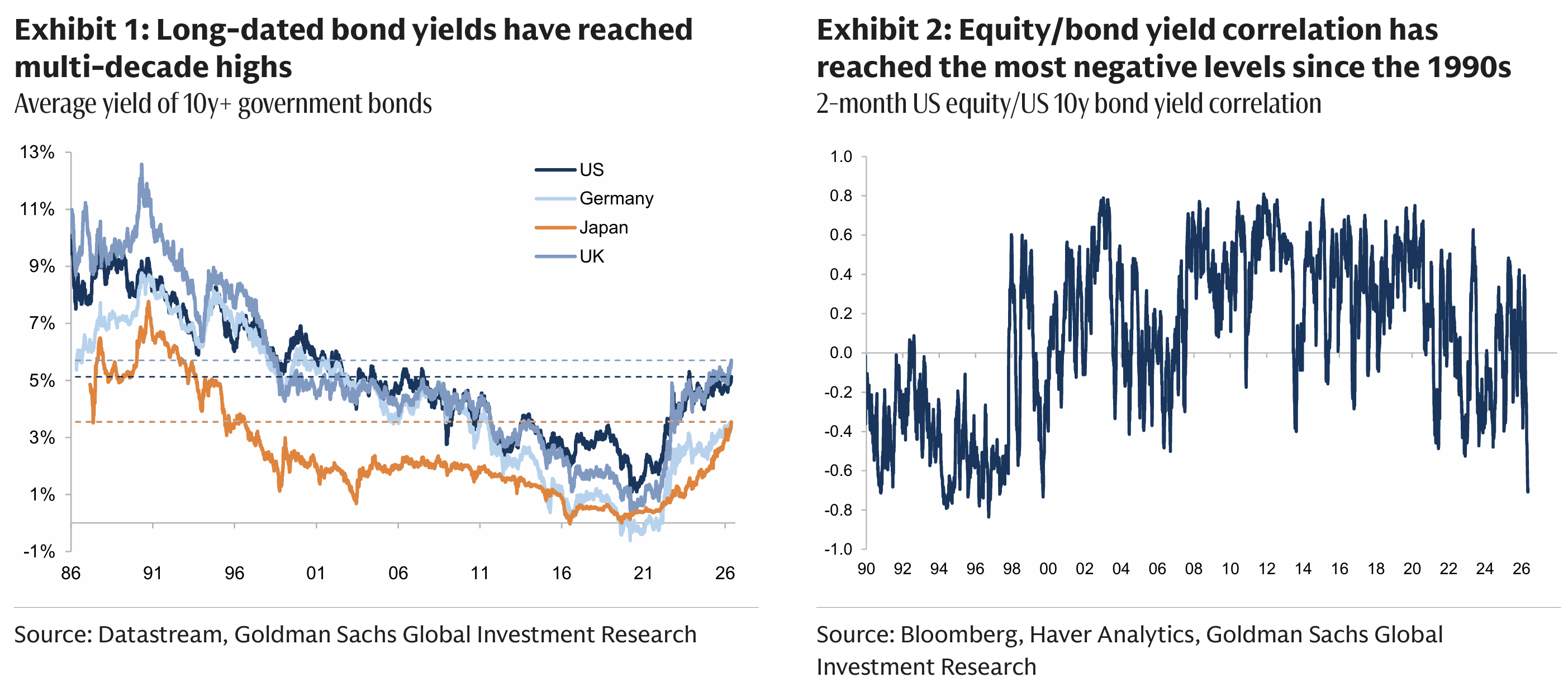

At the core of this sell-off lies the speed and intensity of the yield fluctuations. Goldman Sachs points out that the increase in the U.S. 10-year Treasury yield over the past week has already exceeded two standard deviations, indicating that the previous moderate adjustments have evolved into violent fluctuations.Due to recent geopolitical conflicts causing energy prices to soar, the market has viewed inflation as the main source of macroeconomic shocks, and as a result, the two-month rolling correlation between U.S. equities and the 10-year Treasury yield has turned negative, falling to its lowest point since the late 1990s.

For investors, this extreme negative correlation between equities and bonds means that traditional asset portfolios are facing severe pricing challenges. Historical experience shows that when yields rise due to economic growth, the stock market can often digest risks, but interest rate spikes driven by inflation directly constitute bearish factors for the stock market. Goldman Sachs believes that although U.S. Treasuries are more attractive from a risk premium perspective at present, this negative correlation pattern of both equities and bonds being hit is difficult to dissipate in the short term, and investors need to guard against potential extreme tail risks on the interest rate side.

In response to the current macro environment, Goldman Sachs maintains a neutral stance on equities for both the next 3 months and 12 months in its asset allocation. To hedge against potential equity sell-offs triggered by further increases in U.S. Treasury yields, Goldman Sachs suggests that balanced investment portfolios consider hedging with "equity decline and interest rate increase" dual binary options. In terms of segmented assets, Goldman Sachs expects a negative return of -2.5% for the S&P 500 index over the next 3 months, while maintaining an overweight recommendation for U.S. and UK bonds.

The next market focus will shift to policymaker actions and European macro indicators. As the U.S. lacks significant macroeconomic data this week, the market focus has fully turned to intensive Fed officials' speeches, including public statements by Federal Reserve Governor Waller, Vice Chairman Barr, and local Fed Chair Powell and Barkin. At the same time, the latest inflation data and manufacturing PMI initial values to be released in Europe will also become the core basis for assessing global reflationary pressures.

Content is for reference only, not financial advice.