Macro Panic Subsides, Goldman Warns: Position Risks Are Far from Resolved

Goldman Sachs senior trader Lee Coppersmith issued a warning this week that beneath the calm surface of the current market, there are undercurrents at play.

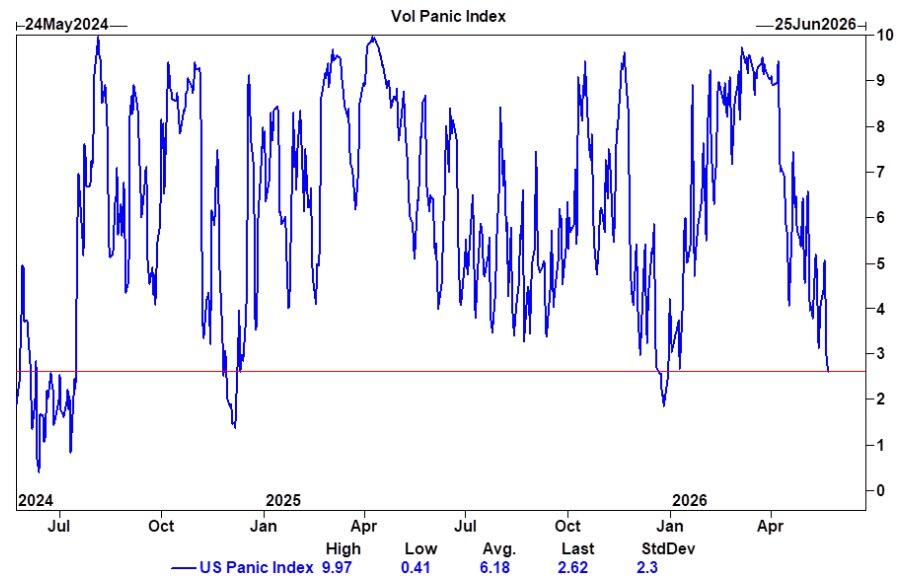

The Goldman Sachs US stock volatility panic index has plummeted from the high levels of 9.5 to 10, which were reached multiple times between March and April, to 2.6, marking the lowest level since the beginning of the year. This indicates a significant reduction in macro-level hedging needs and panic sentiment, but this tranquility against the backdrop of high interest rates, ongoing geopolitical uncertainties, and weak consumer confidence is particularly intriguing.

The market is still generously rewarding the same batch of AI-related stocks. Year-to-date, the Goldman Sachs AI basket index has accumulated a gain of 38%, while the S&P 500 index, excluding AI components, has only risen by 4%. In Coppersmith's view, the market is still essentially dominated by AI infrastructure, semiconductors, and computing power.

Position data is sending a clearer signal. Data from Goldman Sachs Prime this week shows that the total leverage of long-short equity funds in the U.S. stock market increased by 5.5 percentage points in a single week, the largest weekly increase in over three years, while funds massively flowed back into the information technology sector, with both total and net exposure to technology stocks reaching a five-year high. Hedge funds, entering the second quarter, have reached a record 10% allocation to semiconductors, while software holdings have dropped to the lowest since 2019, with a historic quarter-over-quarter increase in technology sector exposure of 853 basis points.

Coppersmith believes that the nature of market concerns has quietly shifted. The previous risk narrative revolved around macro downturns, interest rate shocks, and de-leveraging across the board, but now investors are more worried about momentum disintegration or internal rotation of style factors. He forthrightly states that the market's vulnerability to a systemic downturn in the broad market has significantly decreased, but its vulnerability to cracks in leading segments is on the rise.

In this context, he believes that the hedging value of simply shorting the S&P 500 index has been declining, and momentum hedging or rotation strategies around the fatigue of leading segments may be more attractive. After all, current hedge fund leverage is high, short positions are at historical highs, and incremental risk appetite continues to flow towards semiconductors and AI infrastructure. This structure can be sustained when fundamentals are strong, but once the logic of leadership is shaken, vulnerability will be exposed quickly.

The division within the consumer sector is also worth noting. Last week, hedge funds heavily bought into discretionary consumer goods, while heavily shorting defensive consumer products, with the latter having a net selling scale not seen in over five years. Although consumer data remains noisy, market reactions after Walmart's earnings report have weighed on investor sentiment, but most companies do not point to a substantial deterioration in demand, with discount retail being particularly robust.

Coppersmith also specifically mentioned the subtle structure of the South Korean market. As South Korea is about to introduce single-stock leveraged ETFs, discussions about the liquidity effects have heated up. His core judgment is that the semiconductor leadership pattern has become highly concentrated, and its continued strength is mechanistically creating additional selling pressure through diversification constraints and position limits.

Coppersmith's final conclusion is quite concise: The market has successfully normalized the panic index, but has not yet normalized the leadership pattern, which are two very different things. The real tail risk at the moment may not be a "market decline," but rather the market starting to reward another batch of assets.

Content is for reference only, not financial advice.