Morgan Stanley: AI Expenditures 'Price-Insensitive', Reshaping US Economic Resilience

Morgan Stanley acknowledged in its semi-annual outlook that the biggest surprise of the past six months was not geopolitical shocks, but rather the resilience of the economy to such shocks. Despite soaring energy prices, rising financing costs, and ongoing geopolitical risks, the U.S. economy and corporate earnings have significantly exceeded previous expectations. The report attributes this phenomenon to one key term: inelastic demand.

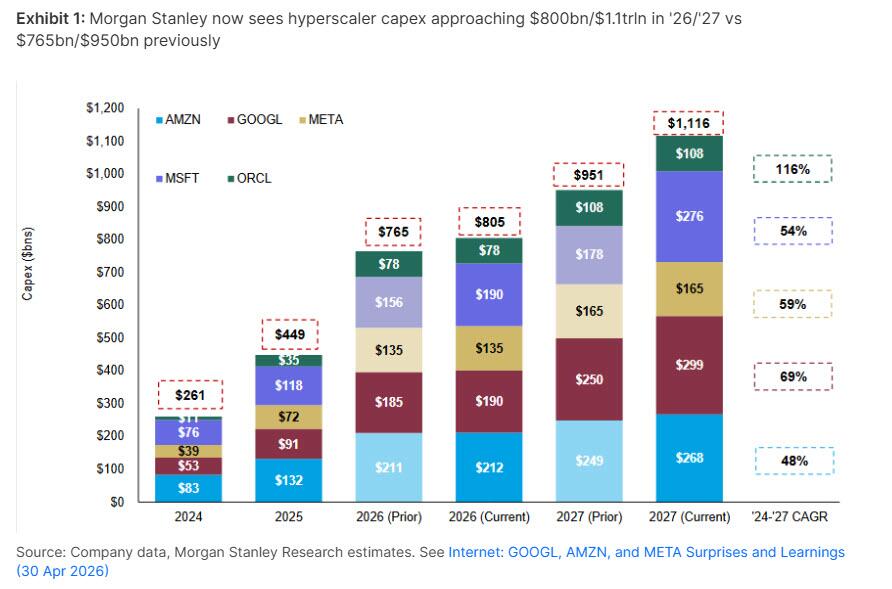

Investment in AI infrastructure is the most quintessential case. A year ago, Morgan Stanley forecasted that U.S. large-scale hyper-scale cloud vendors would spend $433 billion on capital expenditures by 2026; the current forecast stands at $805 billion, with projections reaching $1.1 trillion by 2027 and nearly $1.3 trillion by 2028. What’s more noteworthy is that this acceleration is happening against the backdrop of substantial price increases in key components such as copper, gas turbines, and memory, with the rising costs hardly shaking the tech companies' willingness to spend.

Sheets likens this characteristic to electricity or concert tickets — either a necessity or something intensely desired. For AI investment, it is both: companies are eager to seize the next generation of core technologies and worry about falling behind their competitors. Whether the financing cost is 5.5% or 6%, it is almost irrelevant in the face of this strategic priority. The record-breaking issuance of tech company bonds in 2026 has confirmed this judgment.

This inelastic demand has a direct impact on macroeconomic data. Morgan Stanley has revised its forecast for the growth rate of U.S. business fixed investment in 2026 from 3% to 7%, more than doubling the increase, with AI capital expenditure being the main contributing factor. The consensus forecast for earnings per share growth in the South Korean stock market in 2026 is as high as 235%, behind which lies the benefit logic of South Korea as a core node in the AI supply chain.

Inelastic demand is also reflected on the consumer side. Despite a significant increase in U.S. gasoline prices, gasoline consumption in April was almost the same as the previous year; retail sales excluding oil and gas were better than expected; airfares have risen by 20.7% year-on-year, but demand has not shown a significant contraction.

For bonds and central bank policies, the persistence of this force is a key variable. Morgan Stanley's current base case is that the weight of AI-related categories in the inflation basket is small, and inflation will still recede in the second half of the year, with the European Central Bank, the Bank of England, and the Bank of Japan taking more accommodative rate cut paths than the market expects. However, Sheets also clearly indicated that if inelastic demand turns out to be stronger and more enduring than expected, the forecasts for bond yield declines and central bank dovish shifts will face challenges.

The final question of the report carries weight: what the market really needs to answer may not be whether prices have risen high enough, but whether demand has become too strategic, too essential, or too liquid with funds that they do not care about the price at all.

Content is for reference only, not financial advice.