Philadelphia Semiconductor 'Overbought' Level Approaching March 2000 Level

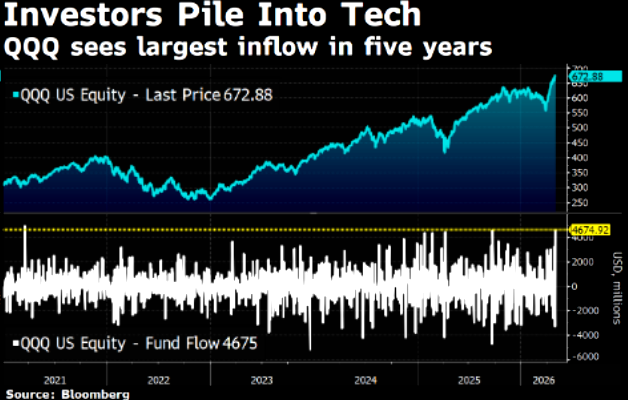

The Philadelphia Semiconductor Index (SOX) weekly RSI has risen to its highest level since the peak of the dot-com bubble in March 2000. Over the past 25 trading days, the cumulative increase has exceeded 50%, and the Nasdaq 100 Index (QQQ) has recorded the largest single-week fund inflow in five years during the same period. The AI narrative continues to ferment, from Goldman Sachs' forecast that global compute consumption will be 24 times the current level by 2030, to the successive increases in tech stocks in South Korea and China, the bubble mirror of this round of market is becoming increasingly clear.

Technicals have entered an extreme territory. The SOX index closed at 11,472.75 points on May 6th, with a single-day increase of 4.48%. The cumulative rise over the past 25 trading days has exceeded 50%, marking the strongest 25-day rolling increase since March 9, 2000. BTIG's head of technical analysis, Jonathan Krinsky, pointed out that SOX's 14-day RSI has risen above 82, the highest since November 2017; the index's deviation from the 200-day moving average exceeds 40%, the largest leading gap since June 2000— "Excluding the special case of March 2000, which is regarded as the largest bubble in modern history, we are in an extreme and unsustainable territory."

Options market sentiment is boiling in sync. The call options for three semiconductor stocks, Micron (MU), Intel (INTC), and SanDisk (SNDK), all had a single-day trading volume higher than the S&P 500 Index (SPY), reflecting the core obsession of the current market. QQQ recorded the largest single-week fund inflow in five years during the same period, and the top ten gainers in the NDX over the past year achieved an average increase of 784%, not only surpassing the annual top ten average of 559% in 1999 but also the 622% before the peak in March 2000.

The fundamental narrative continues to expand. Goldman Sachs predicts that by 2030, consumer and corporate AI intelligent bodies will drive global compute consumption to 24 times the current level; global semiconductor sales and Taiwan's export orders continue to record strong growth; the valuation gap between Chinese tech stocks (KWEB) and QQQ has expanded to historical extremes, and the space for upward price elasticity release is considerable once catching up. The volatility of the South Korean Composite Index (KOSPI) has begun to be passively bid, with the initial signs of upward panic sentiment emerging, but it has not yet entered a full outbreak phase.

Content is for reference only, not financial advice.