Sanctuary Beyond AI: Goldman Sachs Bets on Healthcare, European Banks, and Defense Sector

Louis Miller, Global Head of Goldman Sachs Stock Derivatives and Customized Basket of Stocks, pointed out that the momentum stock sell-off that began in mid-May has marked the largest consecutive decline since 2022. This indicates a relaxation in the market's concentration on core AI assets, with capital beginning to look outward for diversified allocation opportunities.

Overseas AI infrastructure and supply chain segments have absorbed some of the overflow funds. Louis Miller believes that Asian AI transactions have seen significant increases earlier, and the adjustments in May provide a buying opportunity. Goldman Sachs particularly recommends focusing on the Asian AI bottleneck portfolio and the Taiwan AI capital expenditure portfolio. Both of these portfolios fell by about 3% in the previous week, with their constituent stocks possessing strong pricing power in the supply chain.

Against the backdrop of potentially sustained high interest rates, low-quality assets face downward risks. Goldman Sachs data shows that the low-quality stock portfolio, composed of profitless tech stocks, low-profit small-cap stocks, and high-yield bond-sensitive enterprises, has recently shown strong performance, diverging from the trend of the U.S. 10-year Treasury yield. If U.S. Treasury yields cannot retreat to previous levels, this portfolio has more than a 20% downside potential relative to the broader market. In response, Goldman Sachs suggests shorting against the newly introduced basket of profitless non-conventional tech stocks, which excludes overvalued themes such as space, satellites, and quantum computing.

The healthcare sector is seen as a defensive portfolio with very low correlation to AI. Due to a previous lack of clinical breakthroughs and large-scale mergers and acquisitions, the defensive sector has overall underperformed cyclical stocks. However, Goldman Sachs points out that the healthcare industry's absorption of AI (such as AI pharmaceuticals, hospital capital expenditures) is bringing potential dividends, and it has anti-decline attributes during AI stock sell-offs. Among them, the biotechnology sector benefits from the upcoming wave of patent expirations, and strategic merger and acquisition portfolios and the life sciences tools sector have shown signs of order and performance recovery.

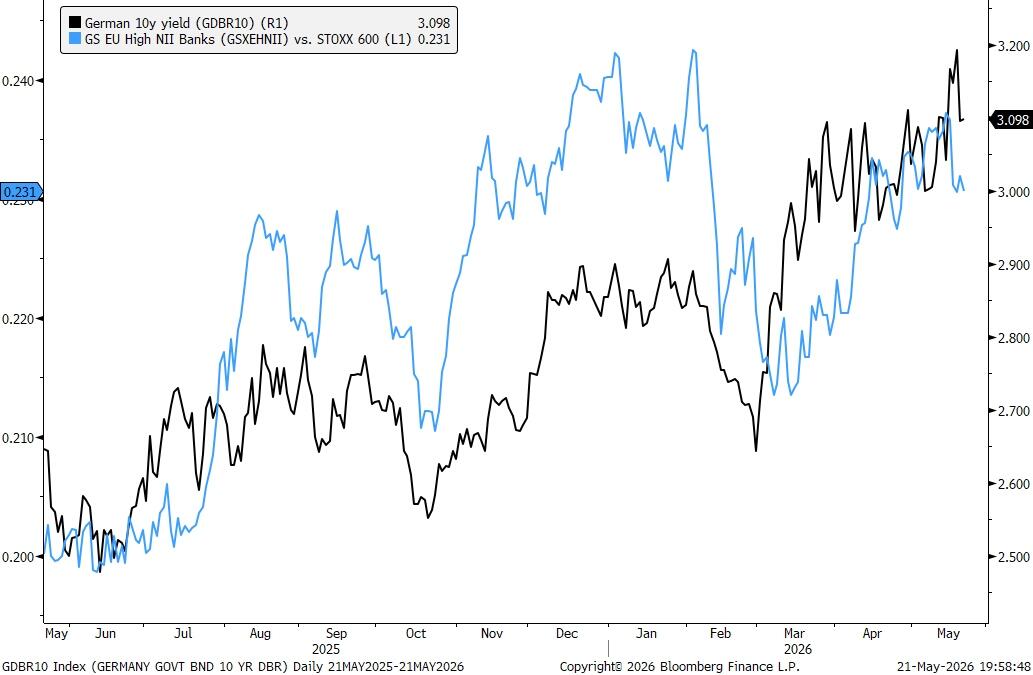

Non-US financial stocks also have the appeal to divert funds, with Goldman Sachs preferring to choose overseas banking assets. In Europe, Goldman Sachs recommends focusing on the European bank portfolio that is most resilient to net interest income under high interest rates and the Greek bank portfolio. In Asia, the recent interest rate hike stance of the Bank of Japan has made the Japanese bank stock portfolio valuable for allocation before the next policy meeting.

The rise in global defense spending is driving a valuation repair in the defense sector. After the initial valuation adjustment and position clearing at the beginning of the year, the price-to-earnings ratio of the European defense portfolio has dropped from 29 times to 23 times, with a potential increase of more than 20% if the valuation is restored to last year's median. In addition, the new mid-cap defense portfolio provides pure exposure to high-tech defense assets such as drones and cybersecurity; the U.S. defense portfolio has also become cheaper due to large-cap beta adjustments, and post-war inventory restocking is expected to bring earnings upgrades.

针对 potential post-war and geopolitical situation easing scenarios, Goldman Sachs indicates options opportunities for low-momentum stock rebounds and the consumer sector. If geopolitical risk premiums recede and the AI craze cools causing a drawdown in the S&P 500 Index, the market's current hedge cost against growth risks is low. Investors can hedge the risks of a decline in the S&P 500 Index and a retreat in interest rates through structured tools such as double-digit options.

Content is for reference only, not financial advice.