Stock Market AI Frenzy Hits the Interest Rate Wall, Cracks Are Widening

This round of AI-driven U.S. stock market rise is colliding more and more head-on with the interest rate market.

The most conspicuous divergence at present is the continued surge in bond volatility while the stock market is still pricing an "almost perfect" environment. The gap between the S&P 500 and the inverse of the MOVE index has widened to an extreme level, with the stock market's performance as if it exists in another world altogether.

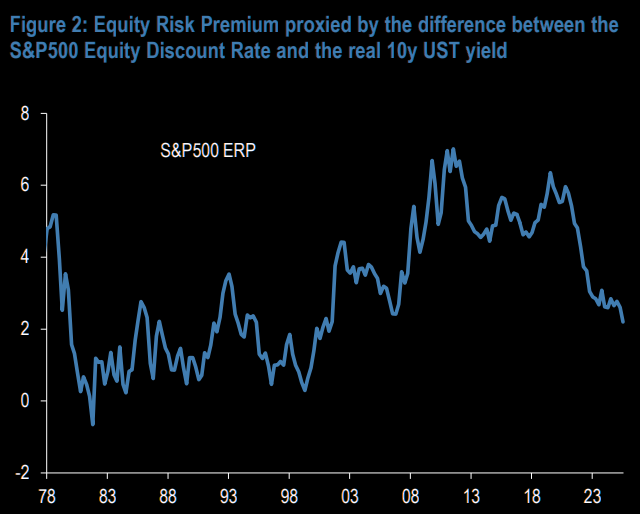

This optimism does not come without a cost—data from J.P. Morgan shows that the equity risk premium of the S&P 500 has fallen to 2.2%, lower than the level in 2007 and the lowest since the financial crisis, about 90 basis points below the long-term average. The lower this number, the more vulnerable stocks are to rate increases, with current U.S. stock pricing leaving virtually no cushion for higher interest rates.

The market's pricing for the Federal Reserve's policy shift remains overly lenient. Deutsche Bank strategist George Saravelos pointed out that if Kevin Warsh joins the Federal Reserve, there will be a substantial upward shift in the distribution of U.S. interest rates, especially against the backdrop of fiscal stimulus and AI-driven inflation rising in tandem. He believes that the overnight foreign exchange volatility定价for the FOMC meeting on June 17th is still too cheap.

The issue of AI inflation is the structural shift that warrants the most vigilance at present. AI is increasingly resembling a classic boom in capital expenditures rather than a productivity revolution. The annualized increase in the U.S. software CPI has exceeded 60%, capital goods inflation has risen to its highest level since the early 1990s, and North Asian AI-related exports are also climbing rapidly, with even Samsung recently issuing substantial bonuses to chip workers. Saravelos clearly stated that AI is becoming a driver of inflation, not a force to suppress it, which is in stark contrast to the market's previous general expectations.

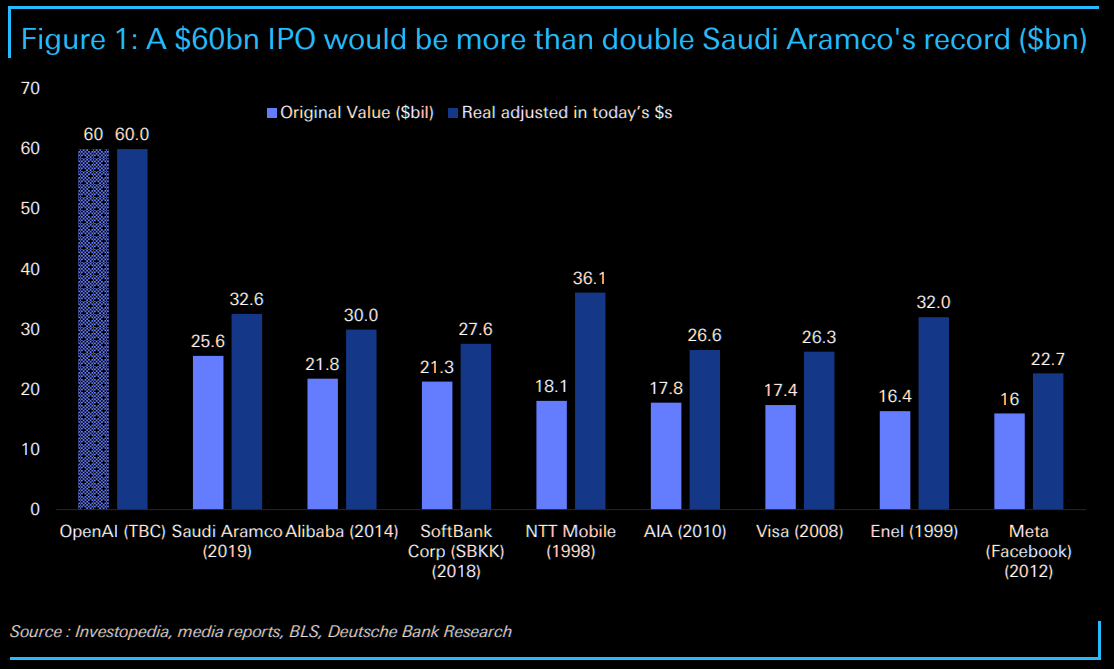

On the capital market front, this year may see the largest-ever wave of AI IPOs. It is reported that both OpenAI and Anthropic are preparing融资of about $60 billion, which would easily surpass the historical record set by Saudi Aramco's IPO even after adjusting for inflation. Deutsche Bank's Jim Reid warned that these two deals could become the most important macro swing factor for risk assets before the end of the year—large-scale financing would draw liquidity away from the market, putting pressure on overall risk appetite.

In terms of capital flow, Goldman Sachs' latest 13-F position analysis shows that active funds continued to increase their positions in semiconductors and reduce their stakes in software during the first quarter. The over-allocation of large mutual funds to semiconductors has expanded to 49 basis points, while the under-allocation to software (excluding Microsoft) has widened to -36 basis points, the lowest since 2012. The overall under-allocation to the "Seven Giants" remains at 723 basis points. Active funds are concentrating bets on AI hardware and maintaining a systematic under-allocation to software and large-cap technology stocks. This also means that once a reversal signal appears in the software sector, the short-squeeze elasticity will be considerable. The Software ETF IGV is currently testing key resistance levels; if it can effectively break through the $94 to $95 range, the golden cross signals of the 21-day and 100-day moving averages have also been triggered, and the conditions for the next round of accelerated increases will be basically ripe.

On the Asian hardware front, SK Hynix has

Content is for reference only, not financial advice.