U.S. Stocks and Bonds Correlation Drops to Zero; Safe-Haven Capital Returns to Fixed Income Market

Bloomberg's macro strategist Simon White stated in the report that the U.S. stock market is currently in an overheated state relative to U.S. Treasury bonds, with capital rotating towards the bond market.

Investors are attracted by the 10-year U.S. Treasury yield approaching 4.70% and the 5.20% on 30-year bonds, causing the long-end U.S. Treasury yields to drop by approximately 20 basis points over the past week. However, when viewed through historical data, U.S. Treasury bonds are still cheaper compared to U.S. stocks.

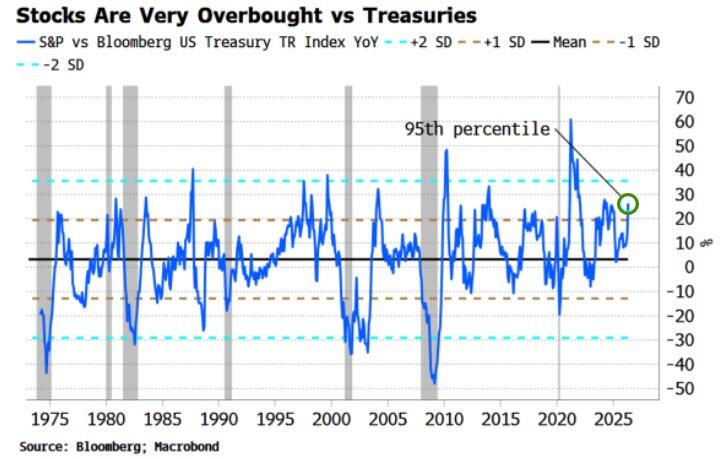

The annualized ratio of the S&P 500 Index to U.S. Treasury bonds has now exceeded one standard deviation, placing it in the 95th percentile of the historical observation period over the past 50 years. Given the mean reversion characteristic of this ratio, the current risk-reward ratio favors Treasury bonds outperforming the U.S. stock market. This valuation mismatch is considered the main driver pushing funds from stocks to bonds.

Actual market capital flows have confirmed this rotational trend; in the past two weeks, the inflow into domestic U.S. stock ETFs has essentially stagnated, while the inflow into U.S. Treasury and corporate bond ETFs has noticeably rebounded. At the same time, net long positions of speculators in stock futures relative to bond futures are also declining.

Previously, U.S. Treasury bonds lost their hedge instrument property due to positive correlation with the stock market, but the structural relationship between the two is changing. The two-year correlation between U.S. stock market and U.S. Treasury price changes has now returned to near-zero. Amidst signs of increasing speculative bubbles in the U.S. stock market, the low correlation is prompting long-term institutional investors to lock in high-yielding U.S. Treasury bonds and reduce stock positions.

Content is for reference only, not financial advice.