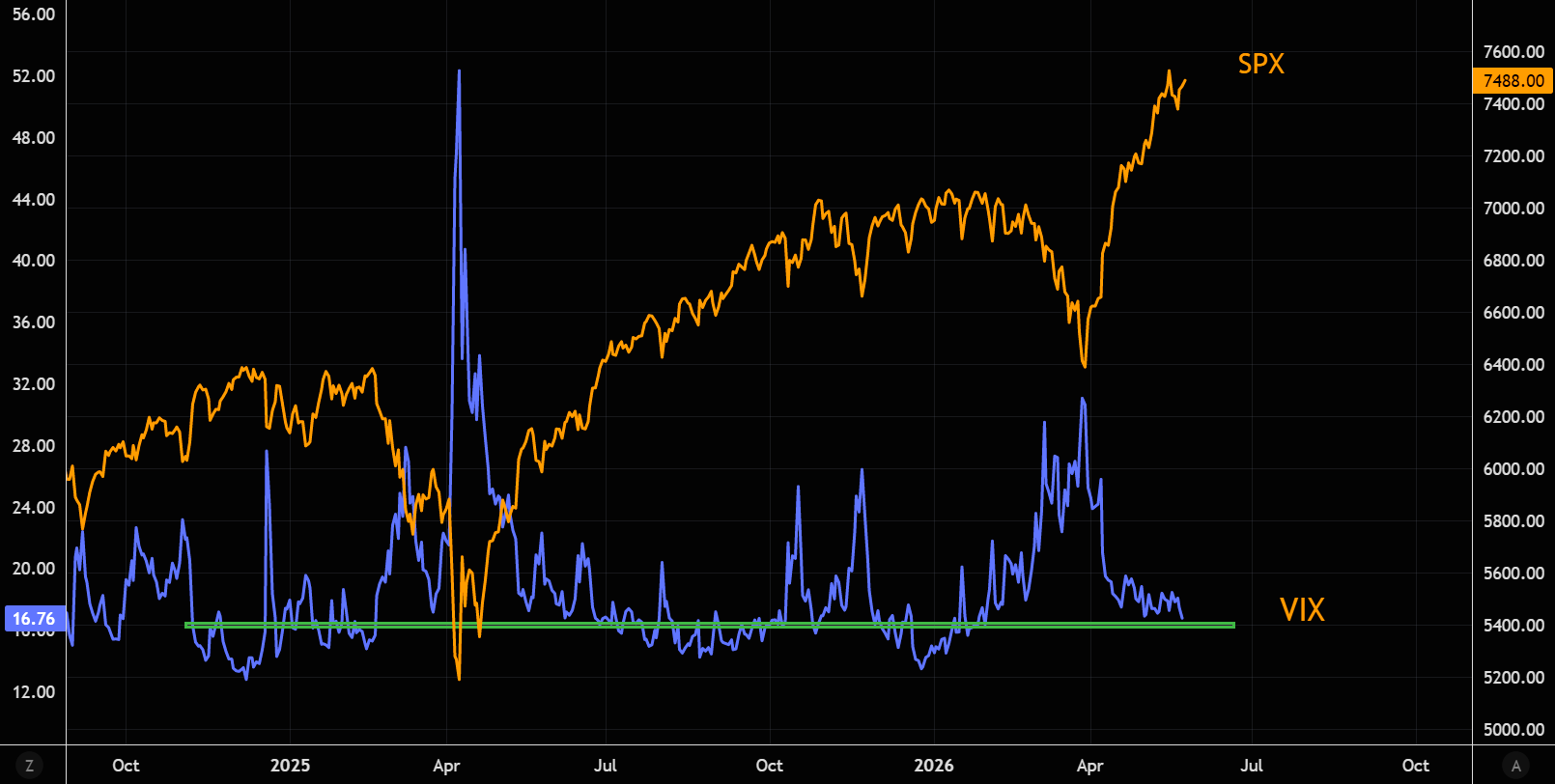

VIX Approaches Natural Bottom, Equity and Bond Volatility Gap Heralds Impending Storm

The VIX has currently retreated to its lowest level since the outbreak of the Iran war, hitting a new low since early February. It is noteworthy that while the S&P 500 index itself is still slightly below its mid-May peak, the VIX has already hit a new low, and the divergence between the two is itself a warning signal.

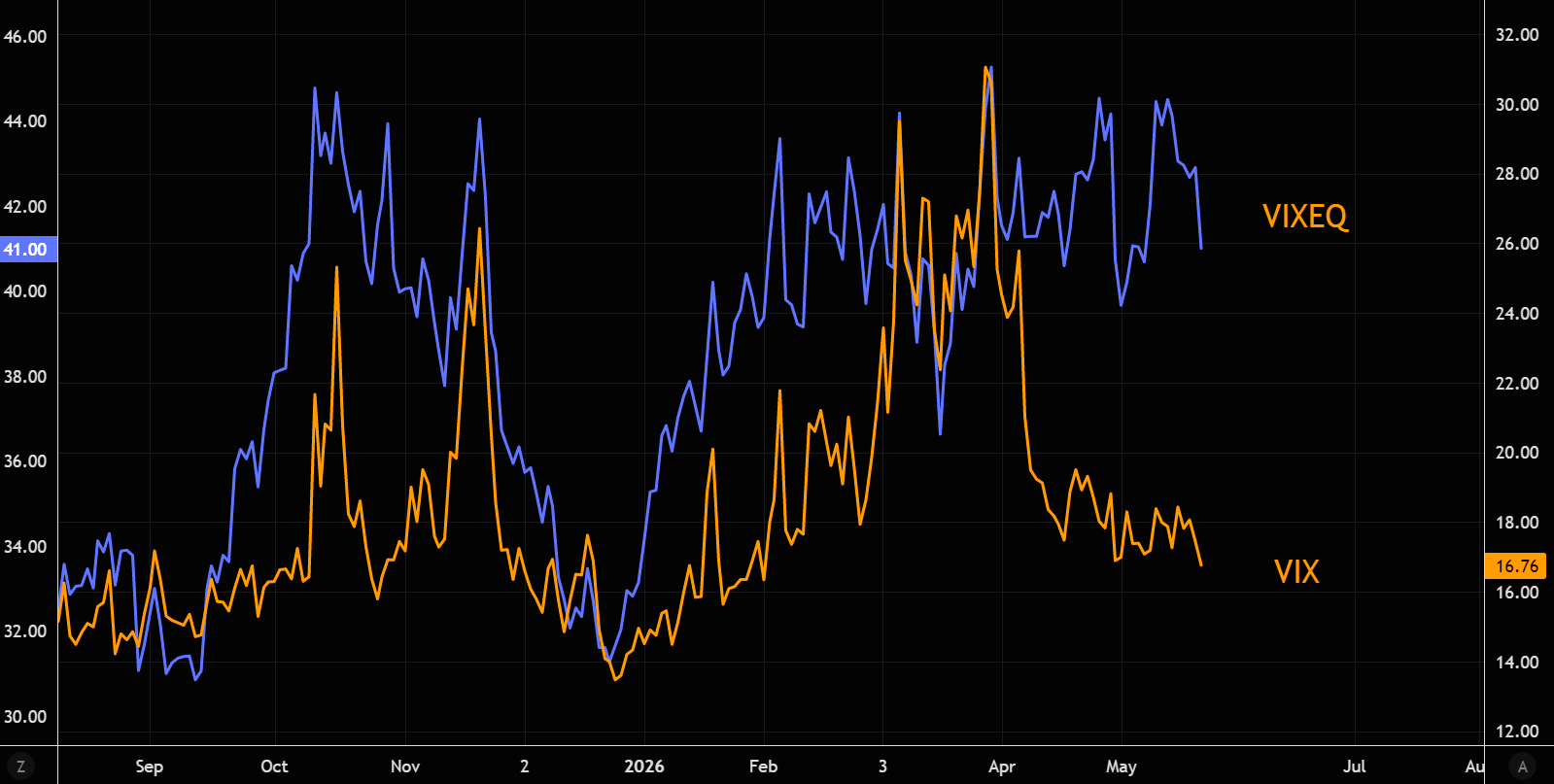

However, not all volatility is decreasing. The single stock option volatility index VIXEQ remains at a relatively high level, with a clear divergence from VIX visible. More critically, the MOVE index, which measures the level of panic in the bond market, has split with the S&P 500 to an extreme level—stocks continue to go their own way against the backdrop of intense volatility in the bond market, and this immunity state is historically short-lived.

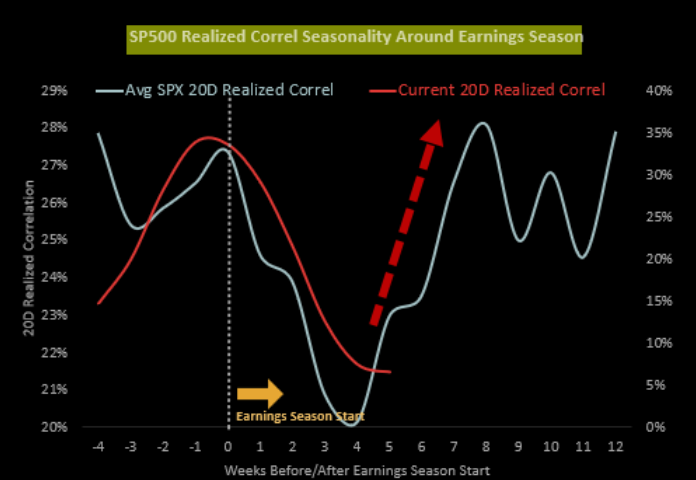

Nomura strategist McElligott pointed out that as earnings season recedes, the market will switch from a micro EPS-driven model back to a macro-driven model. This switch is usually accompanied by a systematic rise in the correlation between individual stocks, and the current implied correlation is at a significantly suppressed level, which means that once the correlation mean reversion occurs, volatility will face a concentrated release.

From a seasonal perspective, the VIX has a historical tendency to have an upward impulse during the current time window, although greater buying opportunities typically occur later in the summer. Against this backdrop, the cost-effectiveness of VIX call spreads is improving—taking the June 20/30 call spread as an example, the maximum payout ratio is about 8 times, and the convexity protection cost is relatively low.

Volatility is often suppressed for a long time, until at some point all assets suddenly move in sync. The current calm may be just the window to reposition protection.

Content is for reference only, not financial advice.