Weak Liquidity Combined with Mega IPO, End-of-Month Pension Fund Sales Impact May Exceed Expectations

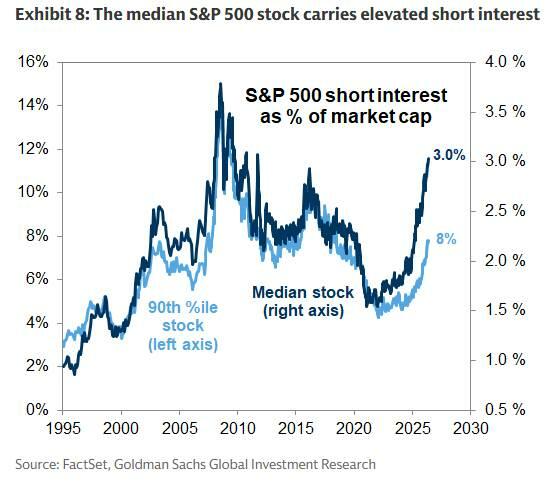

The Goldman Sachs Liquidity Strategy team, Gail Hafif, Brian Garrett, and Lee Coppersmith, pointed out in their latest report that AI trading has performed impressively during the strong earnings season, but the related positions have become noticeably crowded, with the median short interest of S&P 500 constituent stocks reaching 3.0% of market value, the highest level since the end of 2011.

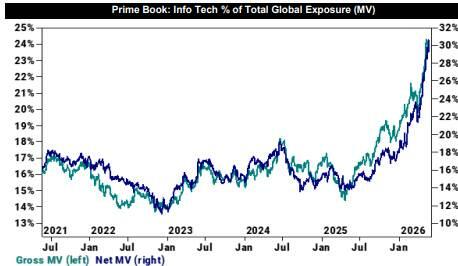

Hedge fund net exposure has risen in tandem with the recent rebound and is now at a one-year high, with total leverage at the 94th percentile over the past five years. The technology sector gained the fastest net buying scale in three months this week, with the total exposure and net exposure of technology stocks accounting for the proportion of the U.S. prime brokerage book both reaching the highest level in five years, i.e., the 100th percentile. Goldman Sachs believes that highly concentrated sector positions mean that the next round of gains might be more "painful" - the risk of short squeezes cannot be ignored.

On the mutual fund side, cash balances as a percentage of assets remain at historically low levels. They touched a historical low of 1.1% at the beginning of 2026 and then slowly rose to 1.4%, but compared to history, it is still extremely limited. With a giant IPO approaching, historically, mutual funds' median cash balance increased by 3% in the month before an IPO and decreased by 2% in the month after, indicating that the "ammunition" available for buying stocks will further narrow.

On the liquidity front, the S&P 500 market liquidity dropped by over $500 million in the past week and now stands at $9.45 million, at the 33rd percentile over the past year, 24% below the average for the year to date. Goldman Sachs warns that liquidity tends to deteriorate faster in the summer, and once the market experiences a rotation beyond AI, the speed of risk transmission will become a key variable, and this technical factor may amplify the volatility of the upward trend.

At the end of the month, pension funds are expected to sell $14 billion worth of U.S. stocks, which is at the 69th percentile of all estimated buys and sells over the past three years, and rises to the 80th percentile when traced back to January 2000, ranking as the 12th largest non-quarter-end sale on record. Goldman Sachs pointed out that this pressure was not apparent in April, but with the current weakening of liquidity, the market impact of pension fund sales could exceed the past.

For the outlook, the Goldman Sachs trading team believes that the market still has room to rise, but the next round of gains are more likely to be driven by short squeezes in lesser-known sectors, rather than the continuation of momentum strategies. If the market cannot achieve a broader sector spread, combined with market makers currently being in a net long gamma position, the market trend may remain moderate until a new catalyst emerges.

Content is for reference only, not financial advice.